Project Value Controls with a Balanced Scorecard (BSC)

by João Miranda

![]() | In Blog - EN|

| In Blog - EN|

Balanced Scorecards are widely used among business and industry, governments and non-profit organizations. However, they are not so much discussed within Project Management and Project Controls, in particular. So, you might wonder why Primaned is writing about them?

If you have been following our blog, you might have read a post questioning the traditional approach of Project Management, focused on the fulfillment of the so-called triple constraint (scope, time and cost). As it was referred, project success is shaped not only by its immediate results but, and above all, by the difference these results will make to stakeholders in the long run, that is, the added value of the project.

This is the basis of a new trend in Project Management. With it, a broader view on projects is established, where these assume strategic relevance. In fact, modern projects are conceived by organizations (public or private) as instruments to carry out their strategies. The value of a project is determined, in this context, by its contribution to the strategy realization and, so, to the whole organization performance.

A bridge must then exist to connect projects to the business and its strategy , that can be attained with Balance Scorecards.

Balanced Scorecards

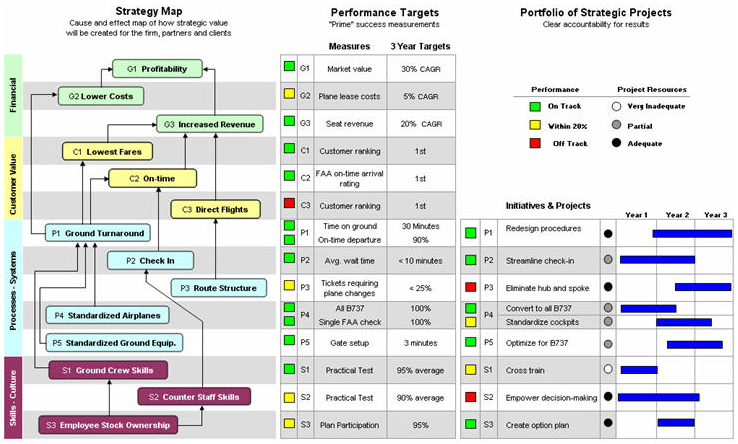

Figure 1 – Example of a BSC (2)

Developed and introduced by Kaplan and Norton in 1992, a Balanced Scorecard is typically defined as a tool for strategy performance measurement, but it is much more than that. It is a methodological framework that helps organizations to think through their vision and goals, articulate them in a strategy and finally translate that strategy into their business operations, as seen in Figure 1.

Without a proper link to execution, strategy becomes a bunch of utopian ideas that fail to be understood and engaged by executioners. So, it is very seldom realized. This is true for both private and public sector, including governments.

Ultimately, with a BSC, the vision of the organization is converted into tangible performance measures, allowing all operations and activities to be aligned with the strategy. Clear objectives and targets are defined, so everyone will be aware what is expected from them. These will act as benchmark to measure the performance against and, thus, to evaluate how well the strategy is being implemented.

The Reasoning behind Balanced Scorecards

In the past, organizations were just concerned on the short-term situation. So, performance was just being evaluated regarding specific financial measures and indicators. Yet, as Kaplan and Norton described, “financial measures tell the story of past events” which are “inadequate, however, for guiding and evaluating the journey that information age companies must make to create future value”. [3]

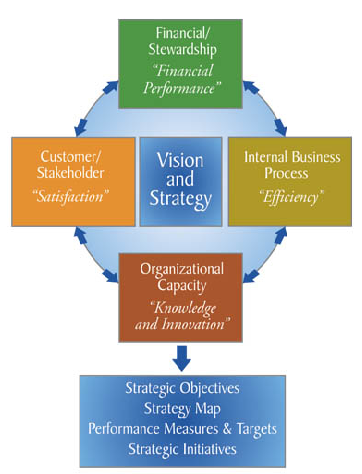

As the name suggests, Balanced Scorecards enabled organizations to balance actual results with less objective measures that drive future performance, from past and current operations and change initiatives. So, their measures cover four different perspectives:

Figure 2: The four perspectives of a BSC (4)

- Financial – Focus on short-term results of actions taken. In case of public entities this is referred as stewardship;

- Customers – The focus is on customer’s satisfaction. Their requirements and needs must be identified and understood and measures must be created, aligned with those. Known as stakeholders’ perspective within public entities;

- Internal Processes – Key business processes and competencies must be identified, excelled and monitored to ensure satisfactory results;

- Organizational Capacity – An organization must be able to enhance and innovate their capabilities to grow. Originally, this was known as Learning and Growth.

With this structure, not only organizations know where they are, but can also look ahead and see where they are going, to assess if they are creating and delivering sustained value.

Balance Scorecards and Projects

From what was exposed during this post, it seems clear the fit between the basis of the Project Management new approach and the Balanced Scorecard rationale – creation of long-term value by linking execution to strategy. Actually, a Balanced Scorecard might be the ideal instrument to “capture, model, analyze, predict, measure, report and inform” value-related data of projects, that needs to be tracked as we track schedule or costs.

Project impacts should be assessed, observing strategic performance measures, against some predefined targets, with a BSC, as any other activity of an organization. These impacts will represent the project value.

As it was exposed in our previous post, with this new trend, Project Controls practitioners were striving to find instruments that allows to capture and deliver value insight. The solution might lie precisely in this classic tool prompted by the business management discipline.

Well, it may seem contradictory to discuss a “new trend” and then suggest an “old” tool. Just look at the dates of the literature references we make. But, in fact, project management getting closer to traditional business management is just part of the essence of this new trend.

In theory it looks good, does it not? But how can we digitize this instrument and integrate within a Project Controls system? This will be shown in one of our next blogposts.

References

[1] Harold Kerzner, Project Management Metrics, KPIs, and Dashboards: A Guide to Measuring and Monitoring Project Performance, 3rd Edition, John Wiley & Sons, Inc. (2017)

[2] Michael E. Porter, “What is strategy”, Harvard Business Review (1996)

[3] Robert S. Kaplan and David P. Norton, “The Balanced Scorecard: Measures that Drive Performance”, Harvard Business Review (1992)

[4] Robert S. Kaplan and David P. Norton, “Using the Balanced Scorecard as a Strategic Management System”, Harvard Business Review (1996)

This blog has been originally posted on Primaned.be on 13 March.